Select the stage for the toolkit

The process of management of contract involves:

- Defining the processes and procedures required to meet contractual obligations;

- Developing strong working relationships between stakeholders;

- Monitoring the performance of the Implementing Business Entity (IBE) to ensure alignment with project objectives and delivery of Value for Money (VfM);

- Identifying, monitoring, and managing risks associated with the project.

From the signing of the PPP agreement to the end of the contract term, the Government Contracting Authority (GCA) undertakes several key activities. These are carried out by a dedicated contract management team, which prepares a comprehensive Management of Contract Plan. This plan outlines:

- Key processes and procedures;

- Roles and responsibilities;

- Escalation mechanisms;

- Integration of service delivery, contract administration, and relationship management plans.

Organized across the various stages of the contract lifecycle, the Management of Contract Plan serves as a strategic tool to ensure that the IBE fulfils its contractual obligations and that VfM is consistently achieved throughout the project duration.

Stage I preparatory activities include the following activities:

- Setting up a management of contract team; and

- Developing a management of contract plan.

An effective contract management team is essential to achieving a project's long-term objectives. This team is primarily responsible for monitoring and reviewing the PPP project to ensure that the private party's performance aligns with contractual terms.

Establishing a contract management team requires careful planning and review. The skillset needed to manage a PPP contract differs significantly from the expertise required to plan, prepare, and negotiate the contract. Managing the risks assumed by the GCA and the associated liabilities is critical to maintaining value for money throughout the project lifecycle and ensuring its objectives are met.

To manage contracts effectively, the GCA must deploy a dedicated team with a deep understanding of project-specific challenges and PPP contract terms from an operational perspective. This understanding is key to determining the optimal team size and the timing and nature of the expertise required. Additionally, Bappenas Regulation 7/2023 highlights the important role of the PPP Node as a technical unit that supports the GCA in ensuring consistent and structured implementation of PPP contracts.

However, the establishment of a team will not, in itself, guarantee that the GCA will be able to maximise the PPP contract’s VfM. It should embed the following characteristics to facilitate achieving and maximising VfM:

- Mandate: The team should have a clear mandate to act on behalf of the GCA and act as the GCA’s representative within the public regulatory environment. A representation may be achieved through internal delegations or institutional arrangements within the GCA or a specific form of legislation/regulation may establish and empower the team (for example: a PPP Node).

- Contractual standing: In addition to a mandate, the team must be empowered within the PPP contract terms to act as the GCA’s representative and to exercise specific powers or rights under the contract.

- Resources: The team must have the human and financial resources to fulfil their mandates and contractual rights effectively and efficiently.

The specifics of the mandate, contractual standing, and resources required will differ from sector to sector and from one project to another. Factors that will influence these functions include (a) scale of a project or program of projects: A useful metric is the value of the assets created by the PPP (b) Administrative complexity of the projects, such as whether they are cross-border or cross-agency in jurisdiction and (c) Extent of GCA-retained risk in the contract (determined by considering the financial consequences accruing to the GCA of a risk materialising).

It is common in PPP projects for majority of the project team of the planning, preparation, or transaction stages to leave the project following the project award or financial close. Getting the management of contract team ready prior to the end of the transaction stage can therefore help with transition and prevent loss of knowledge about the project. Knowledge can be transferred to the management of contract team prior to the exit of the project team.

GCAs should adopt a three-tiered governance structure for management of contract.

- Partnership Committee – Strategic Oversight

- Management of Contract Board – Tactical Coordination (supervisory level)

- Operational Management Team – Service-Level Execution (day-to-day execution level)

This includes defining governance structures and establishing procedures for monitoring and reporting. It also includes understanding risk allocation and who is responsible to manage the risk. Ensure diversity in the three-tiered governance structure to bring various perspectives and skills to decision-making. This includes ensuring women and men are represented. The recommended roles and responsibilities are:

The Partnership Committee is at the highest level; it shall ensure that the project runs smoothly and that the partnership relationship is successfully executed. Communication with all stakeholders is channelled through this committee and any issues that need resolution are addressed at this committee. The Committee shall meet quarterly, however should the need arise, the Committee shall meet on an ‘ad hoc’ basis. The objectives and functions of the Partnership Committee are to:

- Strategically lead the project.

- Provide guidance to ensure that long-term issues are considered and resolved, including outstanding grievances.

- Ensure effective communication and inclusive stakeholder engagement takes place at all levels.

- Ensure that the contract’s objectives are met over the full term of the contract.

- Ensure that an ethos of working in ‘partnership’ is developed and maintained.

- Ensure that the project is aligned with both parties’ (GCA and IBE) business or service plans.

- Consider and report on any changes in legislation.

- Agree on proposed efficiencies and changes.

- Set year-on-year improvement targets, if appropriate and

- Promote best value through the management of whole project life costing through innovation and service improvements.

Partnership committee includes: Senior Leadership Level GCA representatives/ Members; Oversight officials from the Government; Officials from Province & Local authorities; Key members from the Management of Contract Board; Nominees from IIGF; Chairman/ CEO of the IBE; and other key stakeholders like PPP Node, Sustainability Specialist, public representatives, CSOs, etc. The partnership committee should aim to include a diverse and inclusive membership, reflecting the needs of the project sector while ensuring opportunities for qualified women and men.

The Management of Contract Board shall monitor service delivery against service levels & Key Performance Indicators (KPIs) and ensure that the daily contractual matters are dealt with as efficiently as possible. The Board shall meet once a month. The objectives and functions of the management of contract board are:

- Review, discuss and agree on issues arising from the monthly monitoring report.

- Review the payment report and agree on payments due.

- Review the past and future financial performance of the project.

- Resolve issues with regard to production of information.

- Take a forward view of the project.

- Identify efficiencies and necessary changes.

- Record/discuss issues affecting the contract, e.g., compensation events, delays, time extensions, grievances, degree of inclusive stakeholder engagement, safety, access and affordability of services.

- Review areas of conflict.

- Ensure that the partnership board is briefed and actions are taken and

- Promote working in partnership.

Management of Contract board includes: : Supervisory level contract managers from the GCA representing Technical, Financial and Legal wings; PPP Node Officials; Independent Expert; Specialist Consultants; Invited senior representatives from other Government department/ ministries relevant to the project; Senior Officials from the Operational Management Team; and Supervisory level representatives of the IBE. The management contract board should strive to include a diverse and inclusive membership, reflecting the needs of the project sector while ensuring opportunities for qualified women and men.

The Management of Contract Board reports to the Partnership Committee and it leads the Operational Management Team.

The Operational Management Team shall monitor and discuss performance, and manage contractual obligations and any changes driven by the contract or outside the contractual limits that would affect the project. The board shall meet the management of contract team on a regular basis - at least weekly, as a good practice. The objectives for operational engagement are:

- Early identification of issues, including those related to environmental, social and governance (ESG) compliance, inclusive stakeholder engagement, safety, access and affordability of services.

- Produce or review monitoring reports and payment reports (if produced by the IBE).

- Review financial performance of the project and of the contractual parties.

- Discuss and, where possible, resolve minor operational issues, including grievance redressal.

- Ensure that contractual parties are aligned regarding the service level required.

- Promote working in partnership and

- Implement changes when necessary and report back on the same.

Operational management team includes: Field project managers from the GCA representing Technical, Financial and Legal wings; PPP Node Officials; Independent Expert; Specialist Consultants; operational officials from other Government department/ ministries relevant to the project; Field level representatives of the IBE and a representation of CSOs or community where necessary (for example: project that require land acquisition). The operational management team should aim to include a diverse and inclusive membership, reflecting the needs of the project sector while ensuring opportunities for qualified women and men.

The Operational management team reports to the Management of Contract Board.

The governance framework is designed to establish clear lines of authority and allocate responsibilities to ensure efficient management of contract. Each PPP project should ideally be supported by an Operational Management Team, comprising field officers responsible for the day-to-day oversight of project activities. This team works closely with the project implementation unit of the IBE to ensure effective execution on the ground. Their efforts are further supported by consultants and independent experts who monitor project progress and compliance.

At a supervisory level, the Contract Management Board oversees a portfolio of PPP projects on behalf of the GCA. The Board provides tactical support, reviews project performance, and resolves issues escalated by the Operational Management Team. It also liaises with senior officials at the IBE and coordinates with other government departments to facilitate smooth implementation.

At the strategic level, the Partnership Committee offers high-level guidance and addresses disputes that remain unresolved at the Board level. It is also responsible for approving financial decisions and engaging with top-tier authorities within the IBE to ensure alignment with broader policy objectives.

The engagement matrix between the GCA and IBE is as follows:

| Tier | GCA | IBE |

|---|---|---|

| Partnership Committee |

|

|

| Management of Contract Board |

|

|

| Operational Management Team |

|

|

Templates

Job Descriptions

Independent Expert - Terms of Reference

Training is an important part of the GCA’s activity of establishing a management of contract team. Resources involved in the management of contract shall be adequately trained to effectively and competently execute their roles and responsibilities. Inexperienced or less experienced resources pose significant risk to effective management of contract, public sector accountability, and successful project outcomes.

When recruiting and mobilising the team, the GCA shall assess the level and extent of staff training that might be needed. This may depend on the individual’s/resource’s past PPP experience and the knowledge obtained within the field/sector. Therefore, the GCA shall identify initial and ongoing training requirements for all kinds of resources of the management of contract team, and aim to include male and female participants in the training. Additionally, records of training delivered should be kept, with participant lists disaggregated by gender, organisation, and other relevant particulars.

Training curriculum, depending on the resource’s requirements and past experience, may include:

- PPP project or PPP contract-oriented training e.g., Introduction into PPPs & the project life cycle, management of contracts (features, stages etc.), regulatory compliance including ESG and inclusive stakeholder engagement, establishment of a grievance redress mechanism, mobilisation & handover, payment mechanism & its application, risk analysis, performance monitoring, contractual change & variation management, benchmarking, market testing, toolkit usage etc. and

- General training e.g., basic management of contract principles, project & time management skills, negotiation & communication skills, probity & compliance, dispute & issue management, general commercial skills, human resource management and disputes resolution, gender equality and awareness about the inclusion for people with disability, inclusive and respective workplace engagement and support, and relevant computer software.

Templates

Management of Contract Training

Training Requirements

The management of contract plan shall be written in plain language and shall explain the GCA’s duties and obligations, as well as steps to be taken to successfully monitor the IBE’s progress and delivery. The plan shall also provide processes and procedures that need to be followed between the organisational structures and departments. This is typically the case for internal procedures involving different departments within the GCA’s administration, for example the operational management team and accounts department for the payment procedure. In case of projects involving numerous public stakeholders such as waste management and water supply, the scope of the plan may be broadened to manage the interaction amongst key public stakeholders.

The plan shall always be read in conjunction with the signed PPP contract and must be aligned with the processes contained within the contract. The plan shall not be substituted for the contract itself. The plan shall be practical and relevant to both the day-to-day and the longer-term management of the contract. The main components of the plan shall be as follows:

- Steps for taking action: Including the most immediate and critical actions of the Operational Management Team in-charge (Contract Director) and relevant team members while managing the contract. Actions are set out in the context of a clear understanding of the commercial intent of the contract parties and the relevant commercial, legislative, regulatory, and policy background.

- Alignment of resources: The plan shall enable the contract director to identify the resources required to perform necessary tasks and manage the most time-critical and materially significant risks at various stages during the project life cycle.

- Provide support to governance: The plan shall support the GCA’s governance practices including communications, accountability, and decision-making processes.

- Tools and processes The plan shall provide a single point of reference for management of contract tools and processes.

- Adaptability: The plan shall be a dynamic/living document and shall be updated regularly to ensure that it remains relevant throughout the project life cycle.

Templates

Management of Contract Plan

Samples

Management of Contract Plan for a Sample Project

Contents of a Management of Contract Plan

Development of a management of contract plan is one of the first steps undertaken by the management of contract team (Team). The contents of the plan are outlined below:

This is an introductory section covering purpose of the plan, approach, roles, and responsibilities. The Team will detail out in brief the contents of the plan, target audience, users and how the plan is used for implementing the PPP.

In the sub-section on approach, the Team will detail the methodology adopted for preparing the plan and the approach for modifying the plan to reflect changed scenarios during the term of the contract.

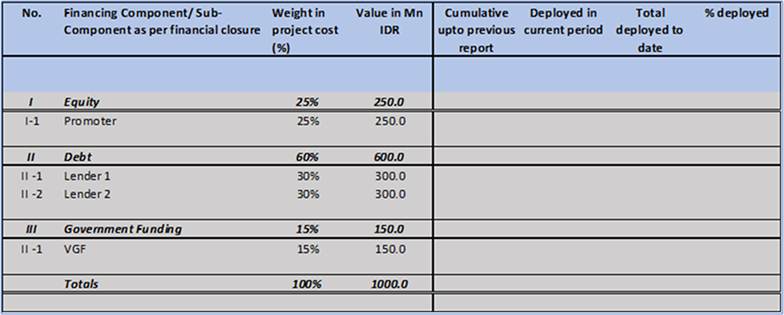

- Details on the project cost and proposed financing arrangements (will be updated after financial close); and is an output of the preparatory stage of the proposed infrastructure provision.

- Conditions precedent stage;

- Obligations of the GCA;

- Obligations of the IBE;

- Revenue structure for the project: User charge/ Availability Payments/ Hybrid/ Others (Land value capture, commercial exploitation, etc.);

- Guarantee and government support arrangements;

- Details on performance security, insurance, etc.

The section should provide details on the objective behind entering the PPP contract, benefits to the GCA from the project and list out the key motivation for implementing the project as a PPP. The Team may refer to the Preliminary Studies and Pre-Feasibility Studies prepared for the project for listing out the objectives of the project.

Key timelines for the project, delineating start and end dates for contract stages – conditions precedent, construction, service delivery, etc.;

The section should provide details on the objective behind entering the PPP contract, benefits to the GCA from the project and list out the key motivation for implementing the project as a PPP.

- Output specification: It should include the performance targets, key performance indicators, benchmarks, target values, penalty system etc.

- Performance monitoring procedure: It is based on the methodology listed in the contract, it includes the details on measuring the performance, timing/ frequency of measurements, modalities for calculations, etc.

- Payment procedure: It includes payment details comprising fixed and variable payments, modalities for adjusting the payment, procedure for levying penalties or payment for incentives, etc. It also specifies the interlinkages with the output specifications.

The performance management system is fundamental to the contract management process since it is the basis of all payments to service providers and any penalties which may be imposed are also estimated through this process based on the terms agreed to in the contract

The Team will need to have a clear understanding of the performance requirements at each stage of the project lifecycle. Understand the performance measurement framework in terms of Key Performance Indicators (KPI) including monitoring of grievance and follow up on issues encountered. Thereafter, a reporting and monitoring framework needs to be put into practise.

The section will also list out the methods for close monitoring of KPIs and institutionalise early warning systems to identify issues for corrective actions including issues or grievance raised via a complaint handling mechanism. During the process of implementation, target KPIs may also be periodically redefined and updated. The modality for such reviews also needs to the included in this section.

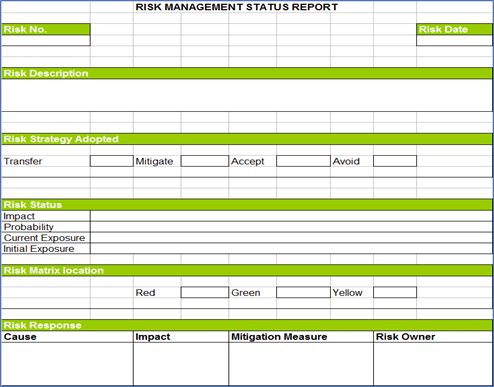

- Risk management plan should identify option for managing risks, allocated responsibilities to individuals to manage such risk. It should also define the procedures to control such risk in terms of escalation procedures. At the same time, the resources required for managing risks in terms of both material and human resources should be defined in the risk management plan. Effective documentation of the plan is critical to it being understood by all stakeholders and implemented efficiently at the time a risk arises. Risk management in terms of monitoring would include not only monitoring the risk identified in the risk management plan but new risks that are likely to arise during the project lifecycle.

- Risk monitoring and reporting structures would depend on duration, size and complexity of PPP projects. As in-case of performance monitoring, risk monitoring also is more critical where the fiscal impact of the project is higher as in case of VGF projects, Availability Payment based projects. The intensity of risk monitoring also depends on the nature of services provided by the project, nature of ESG actions and degree of impacts.

- As important as monitoring of risks is the process of reporting such risks and escalation procedures which should be clearly defined in the risk management plan. Risks may arise from issues or grievances raised via a complaint handling mechanism or similar feedback system established under the project as well as risks identified against ESG risk register tool.

Risk is the likelihood of an event occurring which would cause the actual circumstances and outcome of the project to be different from that assumed during project development phase. The objective of the risk management process is to minimize the probability of occurrence of risk and its potential impact on the project.

Risk management is the systematic process of planning, identifying, analysing, responding to, and monitoring project risks. The risk management process should involve processes, tools, and techniques that will assist the Team in minimizing the probability and consequences of adverse events as indicated and appropriate within the context of risk to the overall project objectives of cost, time, scope, and quality.

-

Risk register

The Team will need to prepare a risk register that lists the risks, sensitivity of the risk (high/ medium/ low), risk bearer, risk monitoring methodology, the risk management strategy adopted, and anticipated revised risk sensitivity (post-strategy adoption, high/ medium / low). The risk register can be adopted from the project risk matrix developed during the pre-feasibility study stage of the project with suitable updates based on its treatment in the PPP contract. The risk register is as follows:

| Risk Type | Sensitivity | Risk Bearer | Risk Monitoring | Risk Management Strategy Adopted | Anticipated Revised Sensitivity |

|---|---|---|---|---|---|

| H/M/L | H/M/L |

| Risk Type | Sensitivity | Risk Bearer | Risk Monitoring | Risk Management Strategy Adopted |

|---|---|---|---|---|

-

Risk monitoring and response tracking

- Dates and action taken to manage the risk

- Action taken when the risk event occurred

- Subsequent action taken

- Update the risk management plan with relevant information based on actual response to risk

Risk monitoring information should be captured in a risk monitoring status report which at the minimum should include:

Risk Monitoring Template should be included as a part of the Contract Management Plan to ensure uniform tracking and reporting of information. The risk monitoring template allocates one page per risk and it maintains a record of that risk during the life of the project. A typical risk monitoring template will include the following details:

-

Risk hierarchy and escalation procedure

This section will need to detail the procedure to be adopted by the Team for managing risks and escalations in case a risk is manifested. The section will provide guidance on how risks can be managed with triggers for escalation based on its categorisation as High/ Medium/ Low.

| Risk Hierarchy Level | Risk Type | Description | Detection Method | Initial Responsible Party | Escalation Threshold | Escalation Path |

|---|---|---|---|---|---|---|

-

Risk management plan audit log

This section maintains a record of risks that occurred during the implementation of the contract and how it was managed. This record helps the Team in recategorization of risks based on its frequency of occurrence, severity, and impact. Sample template includes the following details:

| Risk Name | Details on occurrence | How it was managed | Lessons/ feedback | Entry approved by | ||

|---|---|---|---|---|---|---|

|

Date/ time:

Brief description:

Severity:

Impact

|

Brief details with details on escalations | < Management of Contract Board > | ||||

- Mutual trust based on an understanding of mutual benefit: The parties to the agreement should view the PPP agreement as a mutually beneficial enterprise;

- Understanding objectives: The GCA and IBE must understand and respect the independent objective of each entity and the shared project objectives;

- Open Communication and information sharing: The GCA should foster an environment of sharing information with and obtaining information from the IBE on matters directly or indirectly related to the project.

Relationship management aims at creating a harmonious relationship between the contract parties. The key elements of an efficient relationship are:

The key to developing an effective long-term relationship is the establishment of a collaborative working relationship, together with systems and communications that actively support and enhance the relationship throughout the life of the project.

- Strategic level communication led by the Partnership Committee would focus on discussing the partnership, its management, and any initiatives within it that they could promote or initiate. They would promote the relationship and commitment to a healthy relationship by leading through example.

- Business level communication led by the Management of Contract Board is more formal and structured. Changes to the contract are managed at this level and any issue that arise will be dealt with here should be dealt with through effective communications.

- Operational level where the actual service delivery occurs and is monitored by the Operational Management Team. Day-to-day problems in the delivery of services may be resolved here; if this is not possible, they can be escalated to the Management of Contract Board.

Communication is the essence of a good working relationship. Such communication happens in the following ways:

Successful relationships in contract management are typically spearheaded by seasoned management staff by establishing a collaborative rather than a confrontational approach to contract management.

-

Governance arrangements

The section will detail governance arrangements adopted for the project. It should present the key members of the GCA involved in contract execution and their respective roles and responsibilities. The allocation of roles, responsibilities and delegation of powers will need to align with the three-tiered governance arrangements comprising – Partnership Committee, Management of Contract Board and Operational Management Team. In addition, the section will list the relevant government agencies, independent experts, specialist consultants and other entities associated with the project.

This section will also include details on the counter party from IBE, their contact details, designations, and levels mapped across the three-tiered governance hierarchy, names of the specialist consultants/ project management consultants deployed by the IBE, etc.

-

Contract Review Meetings and communication plan

- Frequency of contract review meetings

- Persons required to attend such Contract Review Meeting

This section should define

Purpose of such meeting should be to facilitate information sharing and enable issues to be red flagged early on and thereby minimizing dispute situations

-

Issue management

Mismatches between the expectations of GCA and IBE and other related parties may lead to issues and disputes during execution which may cause delays in project execution. Timely resolution of any dispute will ensure that user interests are protected and GCA is achieves the project milestones in time.

Identification of issues, recording it and resolution by the Operational Management Team is an important part of relationship management. The process involves maintaining a list of issues observed and the action taken to resolve the issue. The following is a sample of an issue and actions tracker (Tracker). The Tracker includes fields for describing the issue, identifying its impact on the project, allocating a priority for its resolution, assigning responsibilities (GCA and/ or IBE) for resolving it, recording actions taken towards resolving it and status.

Issues and Action Tracker sample:

| Issue ID | Date raised | Raised by | Issue description | Project impact | Priority | Agency to resolve | Action taken to date | Status |

|---|---|---|---|---|---|---|---|---|

| < describe issue > | < in % or kms, area, etc > | H/ M/ L < based on criticality and project impact> | < GCA/ IBE/ other related Parties (Person name, etc)> |

< list actions: meeting references, completed actions, pending items >

< Ideally tagged to a file recording a trail of discussions and documents >

|

< Resolved/ Pending/ Escalated to Dispute Resolution > | |||

The Tracker is maintained by the Operations Management Team. Both GCA and IBE can contribute to the issues as part of their regular review meetings. This Tracker is reviewed by the Management of Contract Board in its monthly review meetings to identify areas of intervention and facilitation.

-

Escalation procedure and dispute management

- The team member observing the issue will highlight concerns to the other party verbally and request intervention to address the issue within [3] days. An issue may also be raised and documented for follow-up by a third party (that may include an individual or group who has/have been adversely affected by the project. They will report to the operational team via an established mechanism for grievances that is accessible through multiple channels (e.g., in person, email, web-based platform, etc;

- If the issue remains unresolved, Senior field team members from GCA (or IBE) can make written note of issue and initiate discussion with to remedy issue;

- If the issue is not resolved within a period of [7] days, the party highlighting the issue can call for a meeting with an agenda to prepare a plan for addressing the issue in the next [15] days;

- If the issue continues to remain unaddressed in the timeframes above, the Management of Contract Board will try to address the issue and put in place an action plan for timely resolution within a period of [15] days;

- If issue is not resolved within timeframes above and those specified in contract (whichever is earlier), escalation procedure will involve issuing written notification to initiate the Dispute Management Procedures starting with Consultation and Mediation as per contract terms;

-

The Consultation and Mediation process will be initiated under the supervision of the Management of Contract Board;

- In case of technical issues – the issue will be referred to the independent expert

- In case of non-technical issues – Negotiations will be led by the Management of Contract Board

- In parallel, the Partnership Committee will be informed of the unresolved issue for its intervention via Fast Track Dispute Resolution if the issue is not resolved while the procedures continue to be in force;

- Issues remaining unresolved will be finally resolved through Arbitration and Conciliation either through Arbitration or by Courts based on the provisions in the PPP contract.

The issue escalation procedure is also sometimes referred to as the grievance redressal mechanism. This includes the following steps:

The following flow chart indicates the escalation flow of issues in a typical PPP contract. Level I is normally led by the Operational Management Team and the Levels II & IV is led by the Management of Contract Board with active participation by the Operational Management Team.

The Partnership Committee will oversee the resolution of the issue while maintaining a channel of communication with the other party to resolve the issue without resorting to implementing the dispute resolution procedures (Level III).

This section on escalation and dispute resolution will be appropriately modified based on the provisions in the PPP contract and the anticipated nature of the grievances.

The objective of this section is to develop and implement contract administration policies and procedures. Such policies and procedures should support the other contract management functions in ensuring VfM while meeting the project objectives.

-

Detailed stage management plans

This section of the plan can be updated in as a project proceeds through the stages. The Team will need to prepare the stage management plan for Conditions Precedent stage at the time of preparing this plan. Thereafter, the stage management plan for Construction stage can be developed during the conditions precedent period and completed as a key stage transition activity before the start of construction on site. For convenience, the detailed stage management plans can be annexed to this Management of Contract plan and annexes can be added as the project transitions to the next stage.

Refer to the sections on Conditions Precedent, Construction, Service Delivery and Transfer stages for detailed contract administration practices to be followed during the stage.

-

Financial administration

Financial administration involves operationalising the payment mechanism which has been defined in the contractual terms and detailed in the contract management plan. The payment mechanism is at the core of the contract, as it puts into financial effect the allocation of risk and responsibility between the local authority and the service provider. Rigorous implementation of payment mechanism which makes appropriate deductions for shortfalls will help incentivise performance

-

Variation management

- Day to day operational variations which could either be a small variation with no significant impact on project outcomes or a larger variation with a significant impact on project outcomes. The process and procedures for managing such day-to-day variations should be clearly laid down;

- Known-unknowns are those events the nature of which is known however the likelihood of when it would occur if it does is an unknown. Example of the same is change in project scope;

- Unknown- Unknowns are those events where both the nature and likelihood of the event is unknown. Example of the same is Force Majeure events.

- Adhering to procedure and process for contract variation specified in the contract;

- Defining clearly the roles and responsibilities of the members of the contract management team involved in the variation management process;

- Documenting in detail all interactions between contracting parties and ensuring effective communication of shared understanding;

- Updating regularly the contract to ensure that it reflects the amended contractual terms

Within contract administration, variation management plays an important role in minimizing conflicts that are likely to arise between contracting parties due to changes in contractual terms.

Variation management involves managing contractual variations during the implementation phase. Such variations could fall in to three basic categories

The success of the variation management process would require the following:

An essential element of variation management is managing transition in the project. The transition happens as the project moves across the stages from conditions precedent stage all the way to transfer stage. The strategies adopted for managing variation will depend on the stage of PPP project and the specific circumstances necessitating such change.

-

Reporting requirements

- What is to be reported

- Format of Reporting – written or verbal

- Frequency of reporting

- Source of Information

This should include procedures and formats for reporting to be done by the Operational Management Team and IBE to the Management of Contract Board and other government agencies. The Team needs to prepare a reporting list covering:

-

GCA risk cover management

PPP contracts include provisions for submission of performance securities, obtaining project insurances, warranties, etc from the IBE. These submissions form the first line of risk cover to a GCA in event of any defaults by the IBE or due to untoward events. The Operational Management Team is required to keep a record of these submissions by the IBE, assess its conformity with the PPP contract, and ensure that the risk cover is always valid. The sample template for managing the risk cover is as follows:

Performance bonds/ security

| Type | Amount as per contract | Dates from/ to | Submission from IBE – details | Accepted, verified | GCA actions/ follow-up |

|---|---|---|---|---|---|

| < Construction/ service delivery/ transfer bonds > | IDR xxx mn | < ddmmyy to ddmmyy > | < Issuing bank/ dates/ amount/ validity > | < Verified by/ details on verification with clause xxx in PPP contract > | < when to initiate renewal/ encashment of security/ reason for encashment/ replacement/ renewal > |

Insurance:

| Type | Cover as per contract | Dates from/ to | Submission from IBE – details | Accepted, verified | GCA actions/ follow-up |

|---|---|---|---|---|---|

| < Contractor all risk policy/ Insurance as per contract/ Climate risk insurance > | IDR xxx mn | < ddmmyy to ddmmyy > | < Issuing insurance agency/ dates/ amount/ validity/ special conditions/ rights of subrogation/ other policy details > | < Verified by/ details on verification with clause xxx in PPP contract > | < when to initiate renewal/ reason for claim/ replacement/ renewal > |

Warranties:

| Type | Requirement as per contract | Submission from IBE – details | Accepted, verified | GCA actions/ follow-up |

|---|---|---|---|---|

| < Certificates on IBE formation/ Board of Directors warranties/ Company secretary certification > | < Details as per clause# > | < submission dates/ details/ special conditions/ etc > | < Verified by/ details on verification with clause xxx in PPP contract > | < when to initiate renewal/ followup/ renewal > |

-

Knowledge management

One of the key objectives of contract maintenance is ensuring continuous availability of project related knowledge and information through the project lifecycle. Knowledge management system and processes should consider the complexity of project, contract duration and the number of stakeholders requiring access to the contract documentation process.

Maintenance of documentation on service delivery and performance to the GCA should include documents related to ESG compliance. For instance, environmental and safety records (compliance documentation), and social compliance documentation (records of consultations and engagement of women and marginalized groups, including indigenous people and people with disabilities in the project at various stages [including their nature of participation and roles], number and nature of grievances and resolutions, and impact of the project on these groups [in all contractual stages]).

To ensure continued service delivery, the contract administration function should define a contract expiry strategy which would come into effect at the end of the contract term. It should define the resources and procedures for ensuring continued service delivery after contract expiry. Developing, testing, and periodically updating a contract expiry strategy is important in ensuring smooth transition of services and continuity of service at the end of the concession term.

-

Recruitment of consultants/ experts

Many PPP contracts require services from specialist consultants to facilitate implementing a project. These include – independent experts, environmental and social specialists, auditors, survey agencies, etc. This section will need to list-out the requirements based on the PPP contract and propose a plan for implementing it.

-

Management of Contract Plan Review

This section should include review procedure for updating the management and the frequency of review.

- Disruption in service delivery not on account of IBE default

- Disruption in service delivery on account of IBE default

- Default by IBE but no disruption in service delivery

- Business Continuity Plan: It aims at mitigating the impact of service delivery disruptions on the key stakeholders. It consists of a series of individual plans for managing each service element of the project. It is important that the contracting parties have a basic understanding of one another’s plans for these events to ensure smooth execution if such a situation arises.

- Step-in Plan: It allows for the contracting party, under exigent circumstances, to “step-in” and temporarily takes control of project facilities to ensure continued service delivery. Provisions for “step-in” are normally defined in the contractual terms.

- Default plan: It sets in when the default clause of the contract is invoked. Since a default plan is typically invoked at short notice and under high pressure situations, it needs to be concise, easily understood, and accessible to all concerned persons.

Contingency plans should assist the GCA is managing and minimizing the impact of risks which have not been effectively contained. Contingency planning is especially important to PPP projects as it may not always be possible to fully transfer the responsibility of service delivery and associated risks to the IBE. The ultimate responsibility of service delivery for PPP projects will still rest with the GCA. The impact to end users because of non-fulfilment of contractual terms by IBE as well as reputational impact to GCA is significant. Hence detailing contingency plans are an essential element of all contract management plans.

Contingencies can arise under the following circumstances:

The contingency plans should define procedures to manage each of these contingencies. Broadly contingency planning consists of the following types of plans:

This section will define how project documents are managed, updated, and stored. Documents for a PPP contract can be categorised into the following. The hierarchy of documents forms an important part in the interpretation of the contract. The documents may be organised as follows:

-

Documents with the highest hierarchy at the time of Preparation Stage:

- PPP Contract and its schedules;

- Letter of award and related communication leading to the formation of the IBE;

- Details on the formation of IBE and related warranties;

- Minutes of Meetings during negotiations;

- Response to the request for proposal and request for qualification submitted by the IBE;

-

Documents with equal hierarchy with above as the contract evolves through the stages:

- PPP contract amendments;

- Correspondence between the GCA and IBE;

- Notices issued, response to the notices and its resolution;

- Right of way, site documentation, assets handover pursuant to various clauses of the contract;

- Various submissions with respect to the contract, example performance securities, insurance, etc;

- Certificates and permissions issued by the GCA with respect to transition of stages, example notification of completion of conditions precedent, commissioning date, etc;

- Regulatory notices and approvals, example – notification to levy user charges

- Permits and approvals obtained from various authorities

- ESG compliance related

-

Operational documents during the implementation of the project and next on the hierarchy:

- Feasibility study submitted by IBE;

- Lender approved financial model;

- Detailed engineering drawings and working drawings;

- Progress reports submitted by the IBE;

- Progress reports submitted by the Independent Expert;

- Permissions and approvals issued by the GCA;

- Reports submitted as per contract;

- Annual financial statements;

- Inclusive stakeholder engagement records;

- Public grievance monitoring, management, and public disclosures

-

Documents connected with the above but entered with other entities:

- Lender agreements and financing package – loan agreement, security documents, tripartite agreements - escrow arrangements, substitution agreement, etc.

- Government support and Guarantee agreements;

- Construction agreement;

- Service/ O&M agreement;

- Facility management agreement;

- Insurance policies;

- Performance bonds;

-

Documents related to formation of the IBE:

- Memorandum and articles of association document of IBE;

- Shareholders agreement;

- Warranty letters issued by the Chairman of the IBE Board of Director and Company Secretary;

-

Documents related to authority of the GCA to enter the PPP:

- Approval from the Minister;

- Legal opinion of the GCA to enter into the agreement;

- Approvals from various authorities as per state support arrangements;

-

Reference documents:

- Project preliminary study;

- Project pre-feasibility study;

- Project preparation documents, including land acquisition and resettlement plans (LARP), and environmental and social impact assessment (ESIA), and gender action plan;

- Procurement transaction documents;

- Pre-bid meeting minutes;

- Details on the bidding process – shortlisted bidders, bidders responding to the RFP, notice to unsuccessful bidders, etc.

- Affordability and public objection to related fees

- Administrative risks, e.g., land acquisition, resettlement, and construction permit

- Local residents and communities objecting to the project / project-affected parties

- Lack of representation across gender, persons with disabilities and/or disadvantaged groups and

- Operational staff, such as teachers in the case of a school project, objecting to the project.

The GCA itself may not be the end-user in several projects. In such cases, the GCA should involve end-users at an early stage because inadequate consultation of stakeholders (such as project-affected parties, persons with disabilities, women, indigenous peoples, and/or specific social or economically disadvantaged groups, consulted during public consultations in the planning and preparation stages in line with the applicable laws, regulations, and ESG standards) can lead to delays in project implementation or make management of contract challenging. It can also result in underestimation of key social or environmental risks and limit the ability of both the GCA and the IBE to mitigate complex or sensitive risks, such as:

It is good practice to establish a stakeholder database disaggregated where possible by gender, disability, and other identities or relevant factors at the start of the project and to update it regularly throughout the contract lifecycle. Furthermore, a dedicated and accessible grievance mechanism and a communication channel can facilitate two-way communication and the dissemination of key or controlled messages. An effective grievance mechanism is one that clearly outlines the steps in the grievance process, is accessible, has multiple channels for reporting (e.g., a web platform, email, in person) and in a language of the target communities (see section on escalation procedure and dispute management). Given that the construction stage is often the most sensitive when opponents may actively challenge the project or influence local sentiment, it is also good practice to appoint an experienced focal point to design and implement an inclusive and culturally appropriate communication and engagement strategy. This strategy should reflect ESG principles and be tailored to reach diverse audiences using accessible formats and inclusive engagement methods.

- Establish contract management team

- Arrange staff transfers/ appoint staff

- Prepare management of contract plan

- Progress report on achievement of CPs

- Conduct regular review meetings

- Notify financial close and transition to Construction stage

- Stakeholder engagement records and documentation

- Conduct quality assurance review

- Prepare performance report

- Review and revise the PPP Contract management plan

- Conduct regular review meetings

- Establish escalation procedure and dispute management (or grievance redressal mechanism)

- Conduct quality assurance review

- Prepare performance report

- Review and revise the PPP Contract management plan

- Conduct regular review meetings

- Ensure functioning escalation procedure and dispute management (or grievance redressal mechanism)

- Evaluate exit options

- Review PPP Contract expiry conditions

This section should present the implementation schedule of various stages in project implementation, the target dates for achievement of the same, responsibility assignment to members of the contract management team and project team and the defined institution budget for each of these steps. These steps may be expanded to take on additional key tasks to reflect the nature of the project.

| Key Tasks | Target Date | Responsibility | Institution Budget |

|---|---|---|---|

|

1. Preparation stage

|

|||

|

2. Conditions precedent stage

|

|||

|

3. Construction stage

|

|||

|

4. Service delivery stage

|

|||

|

5. Transfer stage

|

This section should include detailed stage management plan for the contract stages. For details, refer to detailed stage management plans in Contract Administration.

The Conditions Precedent (CP) stage begins at once after the execution of the PPP contract and lasts until the construction stage begins. This is a critical stage before the PPP contract becomes fully effective and enforceable. In this stage specific requirements or actions must be fulfilled by the GCA and IBE before the PPP contract can move forward to implementation.

The GCA has a set of activities to be completed in this stage. These include: Hand-over encumbrance-free right of way (RoW)/use of land; planning for remaining asset/RoW handover if done in phases; obtaining permissions for use of State/property (BMN/BMD); final approvals for Government support; facilitation of approvals & permits; issuing relevant notifications; appointment of the Independent Expert (IE); and other necessary support arrangements.

Similarly, the IBE’s CP obligations include submission of performance security; achieving financial close; providing legal review and warranties on IBE’s formation; submission of feasibility study; undertaking environmental impact assessment (AMDAL) & related documentation & approvals; etc.

Conditions precedent stage is included in contract as a:

- risk mitigation measure to ensure all critical risks are addressed before major commitments are made;

- readiness check that confirms both parties are ready to proceed with the project; and

- legal safeguard to protect parties from premature obligations if key conditions are not met.

The CP stage ends with a transition to construction stage with notification of effective date of the PPP contract. This is the date when the CPs are satisfied by both GCA and IBE. However, if the conditions precedent is not met within the agreed time limit, then the PPP contract may end automatically, or the parties may renegotiate the timeline or terms with or without levy of penalties or liquidated damages. The parties also reserve the right to waive the CP requirement and go ahead with the notification of effective date.

The approach consists of managing following activities listed in Management of Contract Plan. In addition to managing the activities in the CP stage, the Operational Management Team will need to prepare the contract administration plan for the Service delivery stage as a key transition requirement.

- Monitor receipt of permissions, clearances, land and conditions precedent

- Evaluate of financial models for achievement of financial closure

- Commence of building strategic relationships with all stakeholders and with IBE officials

- Collaborate with IBE to ensure receipt of approvals

- Manage all public communication activities and implement management of contract plan practices

- Managing resource planning activities

- Managing delays in critical activities like land acquisition, financial closure, receipt of permissions/ approvals/ clearances, etc

- Complete conditions precedent actions and initiate start of construction, including developing the contract administration plan for Construction stage

- Extend time based on reasons for delay, review of curative actions, impact on project plan, assess applicability of penalty

The workflow or process for the Operational Management Team for managing CP activities includes the following:

The Operational Management Team will analyse the CP requirements in the PPP contract; allocate the CPs to IBE and GCA; and confirm deadlines and assess dependencies with third parties for its implementation. The following table presents a typical set of CP obligations in a PPP contract:

| IBE Obligations | GCA Obligations | |

|---|---|---|

|

|

|

|

Each party prepares its own CP fulfilment plans based on the requirements. It may need to plan for sub-activities covering documentation, submission to relevant agencies/ authorities, needed approvals, etc. The fulfilment of CPs may also involve extensive engagements with multiple stakeholders.

Example – In-order to achieve financial close, an IBE will need to plan the following activities:

- Prepare detailed project feasibility report, financial model and undertake specialist surveys to finalise project demand, costs, and other project variables;

- Submit the project proposal to a lead lending agency (lead banker) to get the project appraised for financing;

- Provide details on technical, financial, and institutional capability of IBE to implement the project;

- Provide availability and evidence of equity commitment in the project to the lead banker;

- In parallel, engage with IIGF for guarantees and get the project appraised by IIGF;

- Obtain confirmation on budget arrangements by the GCA towards government support in the project (e.g., VGF, grant, land value capture, availability payments, etc.)

- Negotiate with lead banker to finalise the financing arrangements covering debt & equity sharing, lending terms (interest and tenor), financing package, security arrangements, lenders agreements, etc.

- Syndicate funds from other lenders to take part in the financing based on the appraisal by the lead banker;

- Finalise the financing arrangement for the project and submit the entire financing package including details on promoter equity, lending arrangements, lender agreements, security arrangements, escrow arrangements, substitution agreement, guarantee requirements, approved financial model, etc. to the GCA for approval;

- Enter into necessary tri-partite agreements (GCA, IBE and Lead Lender acting on behalf of lenders) for escrow arrangements, substitution/ step-in rights, etc.

To monitor CPs, the Operational Management Team will need to have a good understanding of activities required for completing a CP. They need to be aware of the steps for achieving a CP for the GCA as well as for the IBE and associated third parties. The tracking by the Team will include periodic review of CP status; updating progress; identification of issues and solving issues. The Team can deploy the following Obligations Register Template for CP identification, allocation, planning, monitoring, and tracking.

Templates

Obligation Register

| Obligation | Who? | What? | When? | How? | Status |

|---|---|---|---|---|---|

| Example: GCA to provide land/ ROW for the project | GCA: Contract Manager | Confirm that all land needed for the project has been acquired and that all interests in that land have been extinguished to ease the handover | By [time/date] | Liaise with [ ]; etc. | Contacted [ ] on [date]. [ ] will check status and respond by [date]. |

The Operational Management Team will review the status of achievement with IBE’s counterparty team. The monthly review will include assessing progress on the steps to achieve a CP, identify bottlenecks, resolve issues, and document decisions and actions. The Operational Management Team will also need to provide the IBE updates on the progress of GCA’s CPs to ensure that both parties are aware of the progress of CPs.

Fulfilment of a CP by the IBE will need to be verified by the Operational Management Team and if required by Senior Officials from the Management of Contract Board. For example, the achievement of financial close of a project will need to be verified by the Chief Finance Officer/ Finance Director of the GCA, who is also a member of the Management of Contract Board.

Generally, the Independent Expert verifies the submission made by the GCA and sends its report/ observations on the achievement of the CP. The Independent Expert may consult the agencies involved in issuing permissions/ clearances/ approvals for the CP, visit site (if applicable), review completeness, etc.

The independent expert verified CP report is then evaluated and verified by a suitable authority in the GCA, and its fulfilment is certified to the IBE.

Refer to the checklists for verifying the completeness of a CP fulfilment:

Checklists

Performance Security

IBE Formation and Warranties

Financial Close

Permits and Approvals

GCA Asset Handover to IBE

The Operational Management Team will need to escalate to the Management of Contract Board if there are any delays in implementing a CP. The Management of Contract Board will discuss the issue, find solutions to address the issue. Typically, the party responsible for obtaining the CP provides an explanation to the other party on issues leading to delays and provides a revised plan for achieving the CP. This revised plan may lead to extension in CP period and the parties may agree to amend the CP timelines, if justified. In some cases, liquidated damages/ penalties are levied on the defaulting party for such delays and extensions.

Alternatively, the parties may agree to waive the CP requirement and go ahead with the contract. Such waivers increase the risk in the project and should be accepted only after careful consideration of the risks on the implementation of the project.

CPs remining unfulfilled and not waived beyond prescribed time limits may result in automatic termination of the PPP contract with liquidated damages levied on the party defaulting in obtaining the CP.

The GCA can declare the effective date after all CPs are fulfilled or partially fulfilled after waiving the CP requirements for the unfulfilled CPs. The GCA will need to follow the process prescribed in the PPP Contract. Normally, the process includes issue of formal declaration, notification to stakeholders (lenders, insurance companies, local governments, project affected persons, police, associated departments of the Government, etc.), and documentation to transition to development stage.

Documentation roles of the Operational Management Team will include archiving CP documents, preparation of compliance reports and sending them to relevant authorities. The Team will also need to keep documents, minutes of meetings and other relevant documents to keep an audit trail of the activities in this stage.

A PPP contract becomes effective after the Conditions Precedents (CP) are fulfilled and the effective date for the contract is notified. The construction stage starts on the effective date and ends at the time of Commercial Operations Date (COD) of the PPP project.

During this stage, all parties to the contract and stakeholders shift their focus towards operationalising the agreed PPP contract terms. Parties ensure that risk allocation, compliance with updated financial arrangements, and readiness for disbursement are properly addressed.

The GCA plans for the transition to construction to ensure that the construction stage has a strong and uninterrupted start. The IBE, in turn, fulfills its obligations during the construction stage by constructing the infrastructure asset. In this stage, an Independent Expert (IE) must closely monitor the IBE’s project construction and report to the GCA periodically. The IE supports the GCA and IBE on technical matters related to project construction during this stage.

The GCA reviews progress and performance as per performance indicators developed and specified. These indicators include critical aspects such as physical progress, quality assurance, financial progress, delays & revisions, issues & exceptions, and claims & penalties. Based on results of these reviews, the necessary course corrections or invoking of contractual terms can be undertaken especially if the IBE has deviated from contractual terms.

Construction stage also includes public stakeholder interface. Here, the GCA provides public stakeholders an understanding of what to expect during construction and during service delivery. This is particularly important during construction if the community is inconvenienced by construction activities, for example, increased traffic noise, business disruptions, community relocation etc. and stakeholders’ support is crucial.

The construction stage ends with a transition to the Service Delivery stage. This transition is marked by testing for completion; corrective actions for deficiencies, if any; reaching/certifying COD; notification for collection of fees/tolls/ tariffs; and/or notification for Availability Payments (AP).

The approach consists of managing following activities listed in Management of Contract Plan. In addition to managing the activities in the Construction stage, the Operational Management Team will need to prepare the contract administration plan for the Service delivery stage as a key transition requirement.

- Monitor construction progress, quality and commissioning of the project

- Manage outputs from the IE

- Establish, operationalize communications and manage continuous interactions

- Collaborate with IBE, IIGF and IE to ensure regular reviews and monitoring of construction

- Manage public communication activities and address citizen grievances

- Address gaps in implementation of environmental and social rehabilitations plans and address stakeholder requirements

- Managing delays in critical construction activities, project site related issues, construction quality

- Support IIGF in monitoring key project risks indicators and proactively manage issues to mitigate them

- Complete construction, commissioning requirements and notify commercial operations date; including developing the contract administration plan for Service Delivery stage

- Extend time based on reasons for delay, review of curative actions, impact on project plan, assess applicability of penalty, etc

The workflow or process for the Operational Management Team for managing construction activities includes the following:

This activity ensures that all requirements to commence physical construction on site is complete for the IBE. They include:

- Site handover: The Operational Management Team will ensure the handover of site is completed. Typical handover procedures for site include entering into lease agreements or any other arrangement as per the contract. The handover is recorded in the form of jointly signed hand over documents on the effective date indicating physical transfer of site and risks to the IBE.

- Asset handover: Brownfield projects include taking over GCA assets by the IBE and managing it. Such contracts include provisions for joint inspections and asset inventory checks during the conditions precedent stage. The handover is recorded in the form of jointly signed handover documents on the effective date indicating physical transfer of assets and risks to the IBE.

- Personnel transfer: Some brownfield projects may include taking over specialized GCA staff by the IBE and deploying them on the project. Such contracts include provisions for transfer of personnel and payment of their salaries by the IBE from the effective date onwards. This transfer is also recorded by jointly signed handover documents on the effective date indicating transfer of personnel and risks to the IBE.

- Permits and clearances: The records with respect to all permits and clearances are reviewed and specific actions by IBE towards its continued validity is assessed and noted by the Operational Management Team to ensure continued compliance.

- Site setups: this includes establishing site offices, communication systems, transport arrangements, and allocation of space for the Operational Management Team and IE staff at the site to discharge their duties.

During construction, the IBE submits detailed engineering drawings and working drawings based on the approved conceptual design presented during bidding or conditions precedent stage. The IE will review and approve these drawings on behalf of the GCA for compliance with output specifications.

The IE will keep track of the drawings submitted, approved, and recommended for rectifications. An appropriate register may be maintained by the IE to keep a track of these activities and escalate issues if any non-compliance of rejected/ recommended changes to design is not adhered to by the IBE. A sample template for tracking this activity includes the following, the template is also used to update pending actions by the IBE from the previous reporting periods.

| Received (nos.#) |

Approved without rectification | Rectification recommended | Rectification addressed by IBE | Pending | Remarks by IE |

|---|---|---|---|---|---|

| Reporting quarter – from: _________ to: __________ | |||||

| Reporting quarter – from: _________ to: __________ | |||||

Construction execution

Monitoring the execution of construction is a major activity during this stage. The monitoring is led by the IE and is supervised by the Operational Management Team. The key activity in this stage includes:

-

Assessing IBE’s construction plan: This includes understanding entire construction plan of the IBE. The construction plan is organized into components and sub-components by the IBE, and these components are implemented through specialized contractors or a single EPC contractor. The IE needs to assess the overall construction strategy and plan of the IBE and organise it into a physical implementation plan. A typical physical implementation plan includes the following:

-

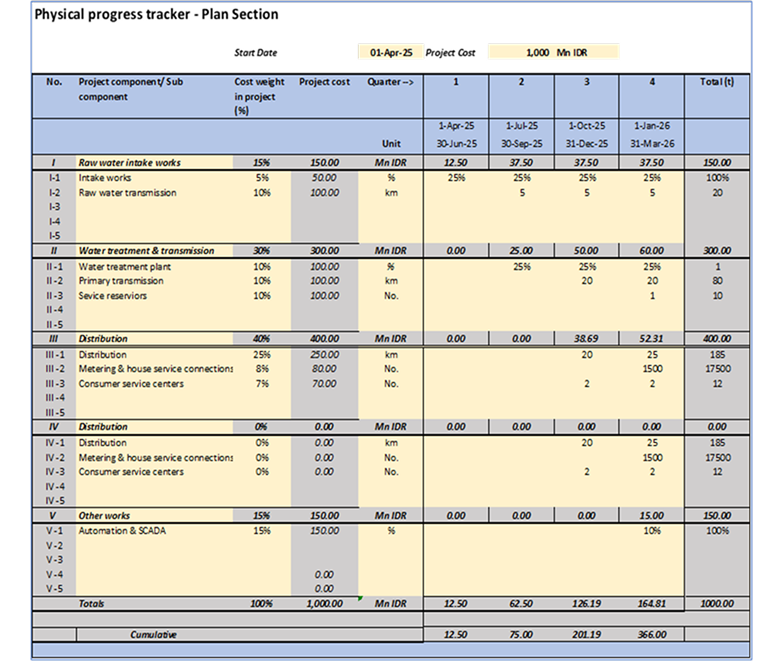

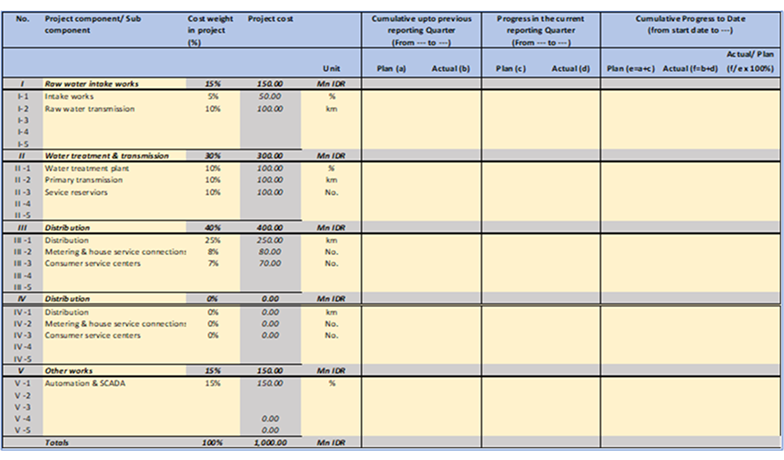

Monitoring and supervision: The IE periodically monitors the construction of the project on site and reviews the actual progress vis-à-vis the above plan. The process includes conducting regular site inspections and reviewing project implementation plans of the IBE. The IE compares the actual progress with the plan to assess the variance and conclude on the pace of construction on site. The IE project progress report may include the following table on plan v/s actual and delays, if any. The IE can also supplement the progress reporting with S-curves for plan and actuals and propose strategies and plans for scaling up construction progress in the event of delays in progress.

Tool

Physical Progress Plan v/s Actuals Monitoring Tool

-

Quality assurance: The IE monitors the quality of construction of the project to o ensure that the final product meets the required standards, specifications, and GCA expectations. The IE in consultation with the IBE and GCA will develop a quality management plan that will consist of quality assurance/ quality control procedures to be followed. The quality assurance procedures in the PPP agreement will be included in the quality management plan. This plan will include inspection and test plans, checklists, third party testing, and quality testing procedures to be applied for key project components. It will also assign roles and responsibilities across the IE team and establish reporting processes on quality testing to the Operational Management Team. The IE may use the following format to report the quality testing during a reporting period

Tests/ type conducted (nos.#) Approved without rectification Rectification recommended Rectification addressed by IBE Pending Remarks by IE Reporting quarter – from: _________ to: __________ Reporting quarter – from: _________ to: __________ Templates:

Quality Management Plan

Site Inspection Report

- Others: The IE will monitor other related aspects of the project concerning health, safety and environment standards and report on non-compliance, if any.

This activity primarily consists of contract administration activities and reporting to the Operational Management Team on periodic basis. The key activities are:

-

Obligations monitoring and tracking: To monitor construction stage, the Operational Management Team will need to have a good understanding of activities required during construction. They need to be aware of the obligations of the GCA as well as for the IBE and associated third parties. The tracking by the Team will include periodic review of obligations; updating progress; identification of issues and solving issues. The Team can deploy the following Obligations Register Template for obligations monitoring, and tracking.

Templates:

Obligation Register

Obligation Who? What? When? How? Status Example: GCA to approve detailed designs GCA: Contract Manager and IE Confirm that all detailed designs and drawings land needed for the implementation of the project has been submitted by the IBE and approved by the GCA based on IE’s review By [time/date] Liaise with []; etc. Contacted [] on [date]. [] will check status and respond by [date]. - Monthly Review and Coordination Meetings: The Operational Management Team will periodically review the construction with IBE’s counterparty team. The monthly review will include assessing construction progress, identify bottlenecks, resolve issues, and document decisions and actions. The Operational Management Team will also need to provide the IBE updates on the progress of GCA’s obligations.

-

Financial monitoring: The GCA will report the deployment of finance for the project to the Operational Management Team and the IE. The financial progress of the project will be recorded in the following manner:

- Risk management: The Operational Management Team with support from the IE will monitor project risks and manage them during construction. They will also coordinate with IIGF and monitor the Key Risk Indicators highlighted by IIGF in their Risk Management Plan and report periodically.

-

Issue management and resolution: The Operational Management Team and the IE will take proactive actions to identify issues and recording it during the construction stage. This will be followed by resolving it in accordance escalation procedures and dispute management in the PPP contract and the Management of Contract Plan. The reporting by the IE will include the following issue tracker as part of its periodic reporting.

Issue description Project impact Priority Agency to resolve Action taken to date Status < describe issue > < in % or kms, area, etc. > H/ M/ L < based on criticality and project impact > < GCA/ IBE/ other related Parties (Person name, etc.) > < list actions: meeting references, completed actions, pending items > < Resolved/ Pending/ Escalated to Dispute Resolution > < Ideally tagged to a file recording a trail of discussions and documents > - Progress reporting: The IE shall prepare a quarterly progress monitoring report on the project. The progress monitoring report should include key details on construction progress, issues (if any) and facilitate the project's implementation. Refer to the template for progress reporting during construction period.

Templates:

Progress Monitoring Report

This phase of a PPP project is critical to ensure that the constructed asset meets all technical, safety, and contractual requirements before it becomes operational. The process includes the following key activities.

- Pre-commissioning testing: In PPP contracts commissioning testing is preceded by a pre-commissioning testing conducted by the IE when the project construction is substantially complete on site. This is conducted for project components and for the entire project. The IE conducts field tests and assesses the readiness of the constructed asset to be put into operations. As an outcome of the testing, the IE prepares a punch list of deficiencies observed and recommend rectification of the identified deficiencies prior to the completion of the scheduled construction completion date. This punch list is formally shared by the IE with the IBE and the GCA for action.

- Punch list rectification: The IBE undertakes actions as per the punch list and rectifies deficiencies observed by the IE during the per-commissioning tests. After completion, it will request the IE to conduct the final construction completion tests for the project.

- Commissioning testing: The IE repeats the testing for certifying construction completion and commissioning the project. It specifically checks the rectification undertaken by the IBE on the punch list items. The IE will then certify that the completion of construction after satisfying itself that all project construction requirements have been met by the IBE. The certification will be reviewed and confirmed by the Operational Management Team prior to the issue of construction completion certificate for the project.

-

Preparatory activities for service delivery: In parallel with the testing, the IBE will submit its service delivery/ operations manual to the IE for its review and finalisation of its service delivery plan. The IE will review the submissions, propose rectifications, and recommend the manual for approval by the GCA. Furthermore, the Operational Management Team will prepare the detailed stage management plan for the service delivery stage of the contract.

Checklists:

Service Delivery/ Operations Manual

The GCA will declare the completion of construction and issue the construction completion certificate for commencing commercial operations. Usually, the next day of issue of construction completion certificate is considered as commercial operations date for the project. Some PPP contracts may include procedures for replacing the construction performance securities with operations period performance securities.

The Operational Management Team thereafter archives construction related documents, prepares compliance reports and sends them to relevant authorities. The Team will also need to keep documents, minutes of meetings and other relevant documents to keep an audit trail of the activities in this stage.

The service delivery stage begins after commissioning of the asset and lasts until the end of the contract term. The transition from construction to service delivery covers the period when the infrastructure asset has been built and is ready to commence operations. Testing and commissioning are distinct activities marking the transition from construction to service operation. The service delivery stage is also called ‘Operations’ or ‘Operations and Maintenance’ stage. Specifically, service delivery begins on the Commercial Operations Date (COD) and continues till the transfer date when the infrastructure provision/asset and project is transferred back to the GCA.

Service delivery activities include

- periodic reviews including service performance reviews, controlling delays & revisions, quality assurance, managing issues & exceptions, and claims & penalties

- managing variations including articulating the need for variations, issuing notification of variations, and approvals & compensations

- Payments during service delivery including operationalising payment processes, invoicing, reviews & approvals, and documentation & release of approved payments.

Even though the IBE is contractually responsible for delivering services, the GCA as the contracting authority remains publicly accountable. The GCA’s role is to monitor the project to ensure compliance with the stated project objectives. Monitoring includes service delivery quality and user satisfaction levels through necessary consumer surveys. If service delivery fails or falls below acceptable standards, the public can hold the GCA responsible, regardless of the contractual arrangements. To that effect, governance, performance management, and risk management are crucial to service delivery.

During service delivery, the Independent Expert (IE) supports the GCA to monitor compliance to the standards specified in the PPP contract. In addition, the GCA reviews progress and performance as per pre-agreed key performance indicators (KPI). Necessary course corrections or invoking contractual terms can be undertaken if deviations from contractual terms by the IBE.

The approach consists of managing following activities listed in Management of Contract Plan. In addition to managing the activities in the Service Delivery stage, the Operational Management Team will need to prepare the contract administration plan for the Transfer stage as a key transition requirement.